Yer a wizard, 'arry! You found the problem again! Here, follow along: - PENSION used to be: this thing where the money was invisible to you and would pay a dividend forever so long as you're alive, with spousal benefits when you die and all that great stuff - PENSION is now: this thing that you got pennies on the dollar for because fuck you, working man - 401(k) used to be: a retirement plan that you and your company poured money into and then the money would pour out when it was time to work on your ship-in-a-bottle collection - 401(k) is now: a retirement plan whose value dropped by 50% in 2000 because you were tech heavy, another 50% in 2008 because you were finance-heavy and sat there like a turd from 2010 until last year because no amount of Fed Reserve gas on the Stock Market bonfire did anything - IRA used to be: a self-guided meditation in building a healthy retirement through your ability to make money on damn near any stock you bought - IRA is now: every bit as shitty as the 401(k) except you can only put 1/6th as much money into it which, fukkit, it's not like there's much to put in anyway Of course, you can buy real estate with your IRA. Or cash it out with heavy penalties to try and make it rich some other way. That skunked the shit out of a lot of people in 2008, too - instead of being underwater on one house they're underwater on five and their retirement was wrapped up in a bunch of assets that depreciated 40% and also cost more than they could afford. Keep in mind: these are 'boomer options here. Punk-ass kids in their 20s and 30s don't have a lot of exposure to any of these options. They've been encouraged to "freelance" and "gig economy" their way to success and unless they've taken it on themselves to set up a self-directed IRA, they have no savings anyway. Which means they aren't pumping money into the market. Which means Bob and Sue's stocks aren't increasing in value because there aren't a bunch of whipper-snappers buying into the market. Also keep in mind: all these options are confusing and Americans get no education in finance whatsoever. We're left to figure it out on our own. The guy who managed the retirement stuff at the first company I worked at out of college thought Mexicans spoke Latin; "why else would they call them Latinos?" You're talking business majors and accounting majors who didn't go on to an MBA; the guys who picked their majors based on having Fridays off are giving you investment advice. Have we set the scene? We've got a bunch of earnest mutherfuckers who, for the past 40 years, have done exactly what everyone told them to do. They've saved as best they can. They lost their shirts several times because they went with the crowd (safety in numbers after all!). The basic marketing ploy for financial services in the US is "you're a fucking moron, do what we say" or "this shit is entirely too simple, even a fucking moron can figure it out" yet they still can't retire the way they were promised. Let's say Hunter found out about this cool thing called Bitcoin in 2014. He bought one for $300. It went up to $600. Cool! It went down to $300. Lame! But it's still worth $300. Then let's say he heard about this other cool thing called Ethereum. he can turn his one Bitcoin into Ethereum at a 2000:1 ratio. So he does. If you're Hunter's dad, you've been scraping your entire life and you're not sure if you're going to be able to retire on your $172,000. If you're Hunter's dad, that $300 of your money made your son two point two million dollars. Do you sense the raw, naked unfairness of it all? Can you taste the anger at the whole of cryptocurrency? Never mind that it's entirely beyond your ken; it's so deeply, divisively unfair. Google IPO'd at $85 13 years ago. With splits, one share at IPO (which you couldn't buy for less than $400; it was a freak show) would be worth about $2200 right now. And if you were the 'boomer that pulled that off you're the envy of all your friends. If you bought $85 of Bitcoin last January it'd be worth over $1000 right now, "death of Bitcoin" or not. And if you bought Bitcoin last January you're probably a millennial. Millennials kill everything. Because if you can't blame the millennials, you have to blame yourself... and the 'boomers really don't see what they can be blamed for. It's not like they did this. It just happened to them. And that's got them so pissed off and scared that they can't even pay attention to how much more fucked the millennials are.What would be a better way to invest into one's retirement int the US?

What would be a better way to invest into one's retirement int the US?

I totally wasn't laughed at here when I suggested adding finances to the curriculum. How much are the millenials fucked? The gig economy? The rising land/home prices?Also keep in mind: all these options are confusing and Americans get no education in finance whatsoever. We're left to figure it out on our own.

And that's got them so pissed off and scared that they can't even pay attention to how much more fucked the millennials are.

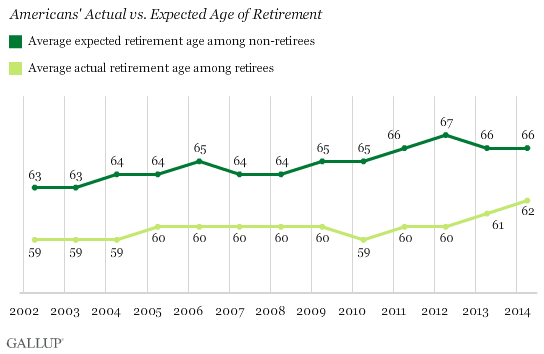

Your dispute in that thread was about "adulting" for want of a better term. How to pay taxes, how to read a mortgage statement, etc. I'll point out that I didn't laugh at you, although I am of the opinion that the fundamental basics are covered. I'll also point out that we're beyond "how to read a prospectus" here, we're at "how to make passive income in an environment where you have neither the leverage nor the knowledge" and that's a bit more than a chapter in Home Economics. Whelp... - there's a social security shortfall that hits in 2034 right now. That's gonna paste everyone under 49 unless something changes. - Older adults didn't do as well as they thought they would so they're staying in their jobs longer. That means kids don't get promoted and the lower end stagnates. - full-time jobs, those with benefits and retirement plans and the like, took a hit during the recession and didn't really recover. That's the obvious shit. Here's the scary one: In your lifetime, the number of wage earners to entitlement users is going to go up 50%. In the US, the "old age insurance" program (social security) has been in the red for six years already. Fundamentally? the average 'boomer is 65 right now. The youngest just turned 50. Over the next 15 years the rest of them will stop working. They'll be effectively removed from the GDP, their spending will go way down, and they'll become a giant drain on health care. Meanwhile all the kids the millennials didn't have won't be moving into entry level jobs because they don't exist and all the taxes necessary to pay for all these old fucks won't be collected because there won't be taxpayers to pay it. But the old people will vote, and they'll have kids who need to pay for them, and the whole of the country will be given over to putting them up somewhere and playing Bill O'Reilly's Greatest Hits for them while the rest of us try to keep the economy churning along with a massive entitlement burden, a reduced labor force and a demographic inversion of pure shit. And retirement? It'll be a thing we used to have. That's how fucked the millennials are.I totally wasn't laughed at here when I suggested adding finances to the curriculum.

How much are the millenials fucked? The gig economy? The rising land/home prices?

I'm sure you can spot the problem — and the solution — yourself. I haven't a clue if it's even possible to gain leverage against the whole stock market on the personal level, but I'm sure we can alleviate the other ailment. ("We"? Not you or me. How many financial specialists are there in the US?) Hence, "classes", not "a handful of lectures". According to your own prognosis, young people today would need a lot of help because their parents would be fucked. Implement one step of the Adulting Program (which is a terrible name, but — "for want of a better term"), and you're in the black. Speaking of which: let me recount. - old folks getting older and leaving jobs, not paying (as many) taxes - young folks getting older and leaving entry-level jobs — and a void in their absence - younger folks working fewer since being fewer, tax income for the state shrinks - older folks will need care for, will receive less since... - everyone sees decrease in health insurance, no one can do a damn thing about it If I follow — and feel free to correct me if I don't — this results in: - young folks getting sicker, which inevitably means decrease in production and, therefore, decrease in GDP - older folks not getting any healthier, but with fewer dollars per illness per head, fewer of the older folks are getting treated, leading to more preventable deaths - younger folks would be forced or lured into working to compensate for the sudden massive void where money used to be 20 years ago - nobody wins, everybody suffers Am I getting near?I'll also point out that we're beyond "how to read a prospectus" here, we're at "how to make passive income in an environment where you have neither the leverage nor the knowledge"

Yeah - adopt a modern, humanitarian system of providing for the elderly. Turning the whole country into stock traders is not a viable solution. There's absolutely zero reason to require people to understand a Bloomberg terminal in order to pay for their retirement. The basic problem is that capitalism has no empathy and empathy is necessary in providing for people in a noncompetitive economy. "How do we take care of a generation of old people" is a civics question yet we're trying to apply market solutions and the shortfall is coming evident on GenX and the millennials.I'm sure you can spot the problem — and the solution — yourself.

That's fair. I was aiming at trying to solve within the current conditions, rather than dealing with hypotheticals. We can teach people how to live with the hand they've been dealt. We can't change what they're being dealt as easily. A curriculum is a summer away. Social changes, especially with a whiff of socialism... you tell me how well that would go. Not saying I'm against it. I'm all for taking care of elderly in a humane fashion. Just saying, as you keep reminding me, that there are real-world obstacles to tackle before the dream comes true.

So this comes full circle: Market investment isn't a zero-sum game: by providing capital to enterprise, enterprise multiplies it and pays a dividend. If the markets can justify their existence, they should always go up. That's the fundamental underpinning of capitalism. Finance professionals (and geeks) separate market success into alpha and beta gains. Beta gains are what you get just by participating in the above. If you throw money at every stock in the market, your money should increase. Beta is what you get just for playing. Alpha gains, on the other hand, are what you get when you make more money than the average schlub. Alpha gains are zero-sum. For you to do better than average, someone else has to do worse. One succinct way to say all market stuff above - percentages diminishing, less returns, yadda yadda - is "diminishing beta gains." You can't educate your way out of that. All you can do is replace your beta with alpha. That's where the name comes from. From a basic game theory standpoint, if you educate all participants so that they can improve their alpha the only thing you will accomplish is making the game harder. It's like computer scams - we've gone from Nigerian princes to spearphishing secondary targets for access to bank accounts. If everyone stayed stupid we'd still be seeing all-caps entreaties for wire transfers. So again: the basic problem is that the baby boomers are outliving the capitalism they created. Most developed nations have some sort of demographic problem but none are as dependent on a free market solution as the United States, which is why I think we're going to have the starkest problems. Social Security is socialism. Medicare is socialism. Frickin' fire departments are socialism. My argument is we need more socialism.

If you ever write or speak about this in public, I'd like to see it: I want to know how well it goes. Not saying it's a bad solution: saying the crowd is tough on that front. Wasn't that one of Bernie Sanders' contention points — that he's a socialist? Because socialism equals communism, obviously, and communism is bad: bad enough that would rather wind up dead than red, isn't that so?Social Security is socialism. Medicare is socialism. Frickin' fire departments are socialism. My argument is we need more socialism.

Yeah - that was an argument against Bernie Sanders. Nonetheless, he just about won the Democratic nomination. Probably would have if the establishment read the tea leaves correctly.