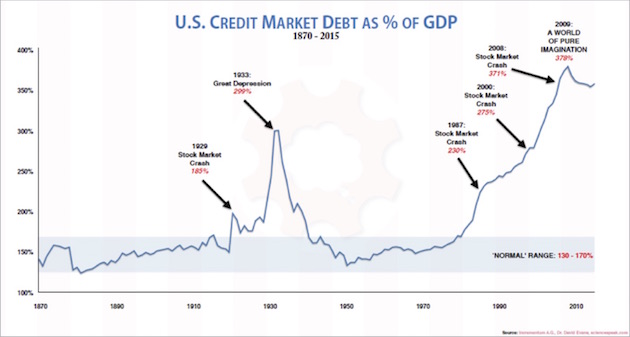

Simply put (a retelling of the New Republic article): 1) Large equity firms have been purchasing retail because it's distressed and therefore an opportunity 2) These firms have been financing the operation of retail through high-yield bond issues which have been largely successful because high yield is almost the last game in town where you can make money 3) High-yield bond issues (retail and otherwise) are no longer attractive to investors because, well, because the bond market is starting to see the writing on the wall, frankly 4) Retailers, who like everyone else close out and reissue bonds rather than waiting for them to mature, can't find any buyers for their bonds which means they can't refinance, which means they can't get any more credit, which means they collapse, which means they take down existing bondholders, which means the utter annihilation of disturbing amounts of capital. The fact that it's 2% means that the bond market will pretty much let it happen. The fact that "retail" means "things people buy" means that there will be ripples. UBS has been freaking out about this for two years now: Note that retail is in the noise on that graph. And that graph is two years old. There are two ways to look at this. On the one hand, people have been chicken littling the sky falling for three years now and we're still alive so maybe credit markets are hunky-dory. On the other hand, maybe we've been piling it higher and deeper those past three years so when it crashes, it's gonna be bad.